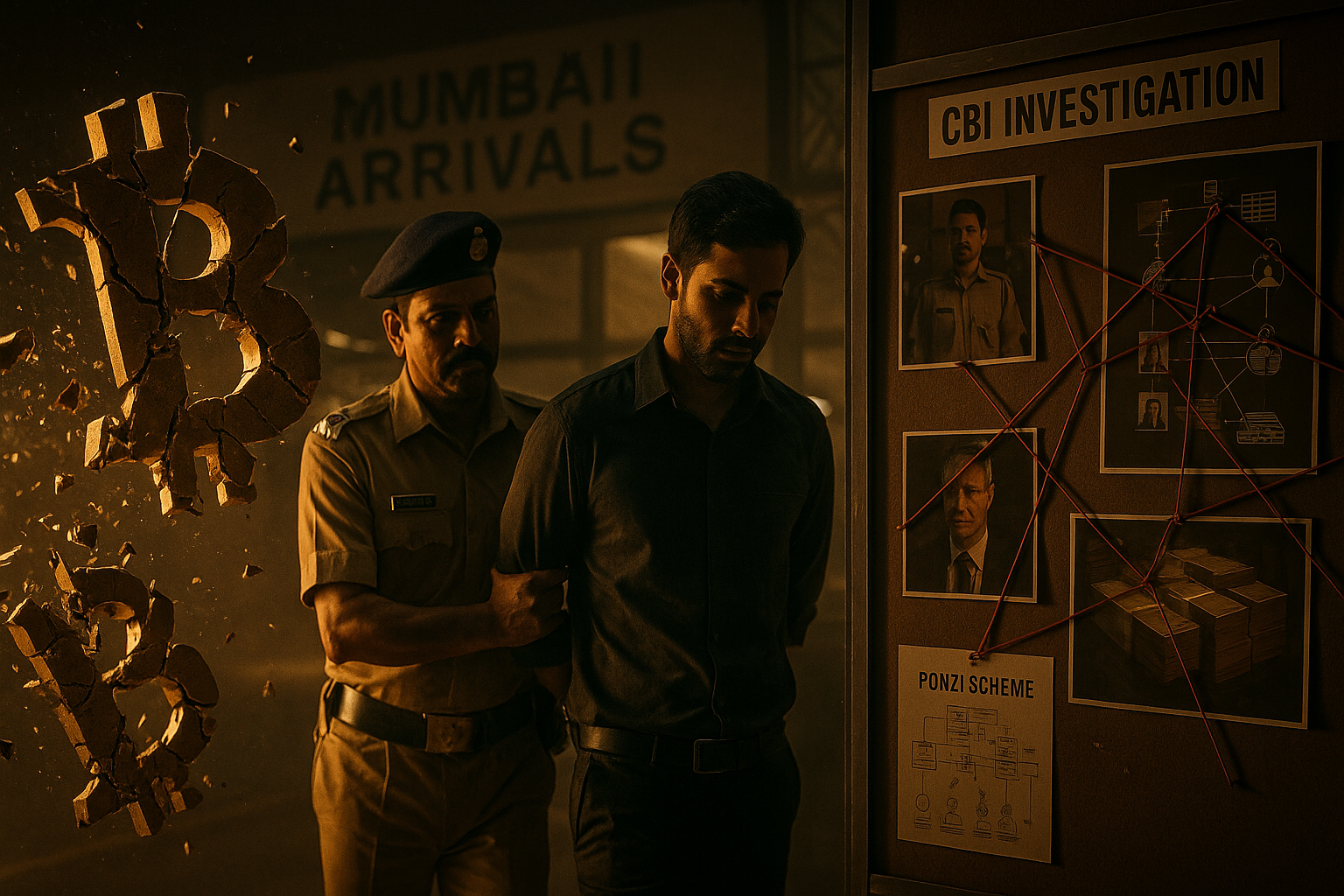

In the early hours of March 22, 2026, Thane Police arrested Sumit Gupta and Neeraj Khandelwal — the cofounders of CoinDCX, one of India’s largest cryptocurrency exchanges — on charges of cheating and fraud. The news broke fast and spread faster, sending shockwaves through India’s crypto community and raising immediate questions about the exchange’s future, user fund safety, and what this means for crypto investors across the subcontinent.

The reality, as it usually is with breaking crypto news, is more nuanced than the headlines suggest. Here’s everything we know, what’s still unclear, and what you should do as a CoinDCX user.

What Happened: The Arrest

On March 22, 2026, Thane Police filed a First Information Report (FIR) against six individuals, including cofounders Sumit Gupta and Neeraj Khandelwal, for allegedly cheating a complainant of ₹71.6 lakh (approximately $85,000 USD).

The complainant, a 42-year-old insurance advisor, alleged that between August 2025 and March 2026, he was approached with an investment scheme promising high returns and “franchise opportunities” linked to CoinDCX. He claims he was lured into investing and lost ₹71.6 lakh in what turned out to be a fraudulent operation.

Both founders were taken into custody and as of the time of writing, the exchange confirmed their arrest while actively disputing the characterization of the incident.

CoinDCX’s Response: “It Wasn’t Us”

CoinDCX moved quickly to distance the exchange itself from the alleged fraud, issuing a statement that strikes at the heart of the case: the company says the perpetrators were scammers impersonating the founders, not the founders themselves.

According to CoinDCX’s statement, fraudsters created fake personas, profiles, and communications pretending to be Sumit Gupta and Neeraj Khandelwal in order to lure victims. The company framed the founders as victims of identity fraud used as bait for a larger scam — not as the architects of the scheme.

This is a significant claim and, if true, would fundamentally change the nature of the case. The FIR names the founders, but the chain of evidence and what investigators actually found will determine whether the arrest holds up.

The exchange also emphasized that CoinDCX as a platform — user funds, trading operations, withdrawal capabilities — is operating normally and is unaffected.

Understanding the Allegations: What This Actually Was

Based on reporting from the Times of India, BusinessToday, India Today, and MediaNama, the alleged scheme follows a pattern security researchers call a “franchise fraud” or “investment opportunity scam”:

- The victim was approached (likely through social media or messaging apps) by individuals claiming to represent CoinDCX

- They were offered high-return investment opportunities and franchise business arrangements “linked to CoinDCX”

- The victim transferred ₹71.6 lakh over roughly 6 months

- The promised returns never materialized

- The victim filed a police complaint naming the founders based on the identities used by the alleged scammers

This type of scam is extremely common in India’s crypto market and has affected users of virtually every major exchange including WazirX, Zebpay, and others. Fraudsters leverage the legitimacy of known exchange names and founder identities to add credibility to their pitch.

The critical question for law enforcement: were Gupta and Khandelwal themselves running this scheme, or were their identities stolen and exploited by third parties?

Are Your CoinDCX Funds Safe?

This is the question every CoinDCX account holder is asking right now. Based on what we know:

Short answer: The exchange is operating normally and user funds appear unaffected.

Here’s the nuance:

The arrest is of the founders on fraud allegations related to an investment scheme external to the exchange’s core operations. This is fundamentally different from:

- An exchange hack or security breach

- Reserve fraud (exchange claiming to hold assets it doesn’t)

- Regulatory shutdown order

- Exchange insolvency

The exchange itself is a regulated entity in India (registered with the Financial Intelligence Unit under anti-money laundering rules), and the arrest of founders doesn’t automatically freeze or affect exchange operations.

That said — anytime key leadership is arrested at a financial institution, risk increases. Here’s how to assess your exposure:

Lower risk indicators:

- Exchange withdrawals are processing normally

- No regulatory shutdown order from FIU-IND or RBI

- CoinDCX has published a clear statement on the situation

- The fraud allegation is relatively modest in scale (₹71.6 lakh is not existential for a major exchange)

Higher risk indicators to watch:

- If Indian regulators (FIU, SEBI, ED) begin investigating the exchange’s books directly

- If withdrawal limits or processing times change suddenly

- If the exchange goes quiet on communications

- If the founders are held for extended periods or additional charges filed

Our recommendation: if you have significant holdings on CoinDCX, it’s prudent to withdraw to a self-custody wallet while the situation develops, not because the exchange is necessarily compromised, but because uncertainty is always a risk factor in crypto.

India’s Crypto Regulatory Context

This arrest doesn’t happen in a vacuum. India has been steadily increasing regulatory pressure on cryptocurrency exchanges and operators over the past three years.

The Enforcement Directorate (ED) has been active: WazirX faced an ED investigation in 2022-2023 related to FEMA (Foreign Exchange Management Act) violations. Multiple exchanges have been scrutinized for KYC compliance gaps.

FIU registration became mandatory: India’s Financial Intelligence Unit required all crypto exchanges to register as “Virtual Digital Asset Service Providers” (VASPs) in 2023. Exchanges that didn’t register were forced to block Indian IP addresses.

Tax policy has been aggressive: India introduced a 30% flat tax on crypto gains and 1% TDS on transactions in 2022, one of the world’s harshest crypto tax regimes. This drove significant trading volume offshore — but the regulatory infrastructure remained.

The broader pattern: India’s government has consistently signaled it wants crypto regulated, not banned. But “regulated” means increased scrutiny of exchanges and their leadership. The CoinDCX founders’ arrest, regardless of its ultimate outcome, is a signal to the industry that founders are personally liable for how the exchange’s brand is used — and potentially for how it’s run.

The Broader Pattern: Exchange Executive Arrests

The CoinDCX situation joins a growing list of high-profile crypto exchange executive arrests globally:

| Who | Exchange | Charges | Outcome |

|---|---|---|---|

| Sam Bankman-Fried | FTX | Fraud, conspiracy | Convicted, 25 years |

| Changpeng Zhao (CZ) | Binance | AML violations | Pled guilty, $4.3B fine, stepped down |

| Do Kwon | Terra/Luna | Securities fraud | Extradited, facing trial |

| Arthur Hayes | BitMEX | BSA violations | Pled guilty, probation |

The pattern matters: exchange founders are increasingly personally liable for platform conduct and, as the CoinDCX case illustrates, even for third-party scammers who exploit the exchange’s brand.

For investors, this underscores a fundamental crypto principle that bears repeating: exchanges are counterparty risk, not safe storage.

What Crypto Investors Should Do Right Now

If you have funds on CoinDCX:

- Enable withdrawal notifications — turn on email/SMS alerts for any account activity so you know immediately if something changes

- Verify withdrawal processing is normal — test a small withdrawal to confirm the system is working

- Consider moving significant holdings to self-custody — hardware wallets (Ledger, Trezor) or a well-secured software wallet where you hold the private keys

- Don’t panic sell — rushed decisions during news events often result in poor outcomes; assess the actual risk before acting

- Monitor CoinDCX’s official channels — twitter.com/coindcx, blog.coindcx.com for official updates

To protect yourself from investment scams like the one alleged here:

- CoinDCX and its founders will NEVER DM you about investment opportunities — this is true of every legitimate exchange

- Verify everything through official channels only — coindcx.com, verified Twitter/X accounts with checkmarks

- “High returns” + “franchise opportunities” = scam — no legitimate crypto exchange offers this

- If someone contacts you claiming to be an exchange founder, it’s a scam — document it and report it

- Use the exchange’s official support channels — not Telegram groups, WhatsApp, or DMs

How to Assess Exchange Risk in General

This case is a good opportunity to review your overall exchange security posture. Here’s a framework:

Custody risk — Where are your assets held?

- On exchange = counterparty risk (exchange holds keys)

- Self-custody = your risk (you hold keys, you’re responsible)

- Rule of thumb: only keep on exchange what you’re actively trading

Regulatory risk — Is the exchange regulated?

- Look for FIU registration (India), FinCEN registration (US), FCA authorization (UK)

- Regulated exchanges have compliance obligations that provide some protection

Transparency risk — Does the exchange publish proof of reserves?

- Post-FTX, major exchanges publish regular attestations

- Check if CoinDCX publishes reserve data

Legal risk — Are there active investigations?

- Use Google News alerts for “CoinDCX legal” or any exchange you hold funds on

- Monitor the exchange’s official communication channels

Liquidity risk — Can you actually withdraw?

- Periodically test withdrawals, especially of larger amounts

- Check for any withdrawal limits or unusual processing times

Bottom Line

The CoinDCX founders’ arrest is a developing story with significant uncertainty. The exchange’s claim that scammers impersonated the founders is plausible — this is an extremely common fraud pattern in India’s crypto market. But until the investigation concludes, the situation carries elevated uncertainty.

User funds appear safe and withdrawals are processing normally as of writing. That can change — follow official channels and be prepared to move to self-custody if the situation deteriorates.

What this story really reinforces: crypto exchanges are not banks, are not guaranteed safe storage, and are operated by humans who face legal and operational risks. Self-custody isn’t just ideologically pure — it’s the only way to eliminate exchange counterparty risk entirely.

Keep your portfolio’s exchange exposure proportional to your risk tolerance, maintain self-custody for long-term holdings, and stay skeptical of any investment opportunity that comes to you via DM or messaging app, regardless of who it claims to be from.

We’ll update this article as more information becomes available.